The information in this article has been corrected.

As reported today by Adam Pagnucco of Seventh State, the Montgomery County delegation (the elected officials who represent MoCo in the state capital) overwhelmingly defeated a proposal by Delegate David Moon (D-20) to close a long-standing property tax loophole for county clubs.

Current law allows country clubs with golf courses to enter agreements with the state to be taxed at a substantially lower rate than regular properties. The failed bill would have gradually phased out these agreements over ten years.

According to the non-partisan Department of Legislative Services, removing these agreements completely would increase the County budget by approximately $10 million dollars per year. This estimate doesn’t seem very far off might be under-estimating the amount by an order of magnitude, since based on the analysis below, this tax loophole can allow a single country club can save over half a million ten million dollars per year in property taxes.

As a result of these agreements, the local tax burden gets shifted from country clubs onto everyone else. The effects of this policy are particularly painful this year, as the County is facing a $120 million shortfall.

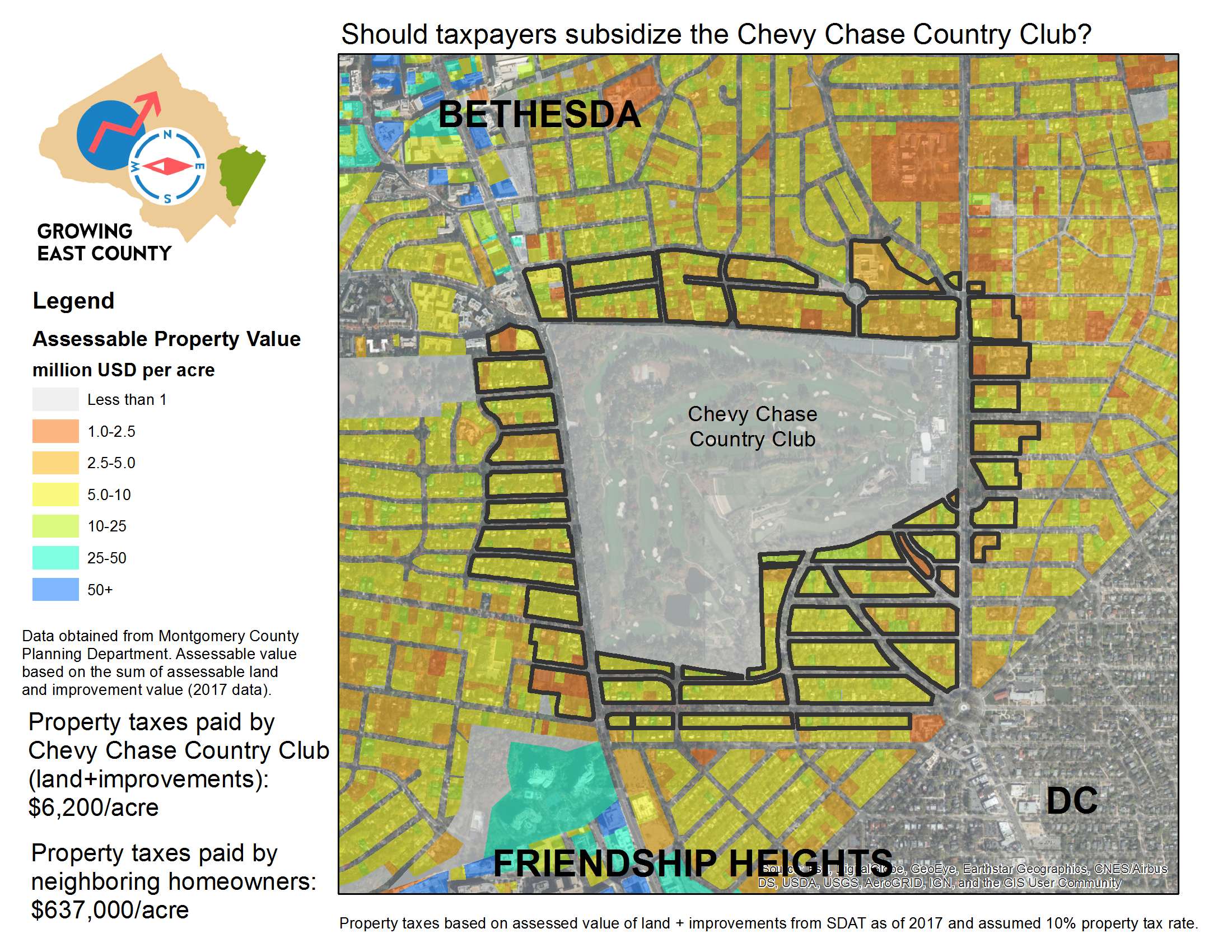

Below is an analysis of how the Chevy Chase Country Club is essentially getting a subsidy of $630,000 per year as a result of not getting taxed the same way as neighboring properties. Get ready to #dothemath…

Case Study: Chevy Chase Country Club

{kind=link}

The map above shows the total assessable property value (land plus improvements) on a per-acre basis in Chevy Chase.

This analysis will compare the Chevy Chase Country Club to a similarly-sized area consisting of 776 parcels (mostly single-family detached homes) within approximately 500 feet of the Club.

The properties encircled with the black borders occupy 180 acres. Their total assessed property value is $1,146,894,000, which equates to $6,371,633/acre. Assuming a 10% 1% rate, these properties generate $637,163/acre $63,716/acre in property tax revenue for Montgomery County per year.

The Chevy Chase Country Club is slightly larger (190 acres) and has an assessed value of $11,713,100, which equates to $62,023 per acre. Therefore, they pay about $6,200/acre/year $620/acre/year, which is $630,000 $63,000 per acre less than the 180 acres nearly 800 homes immediately surrounding the club.

On a per-acre basis, the tax loophole for Montgomery County country clubs allows them to pay as little as 1% in local property taxes than surrounding homes. The total amount of annual property taxes for the assessed value of the 190 acre country club is $117,131. When comparing that amount to the $11,468,940 in taxes owed by the surrounding 180 acres, it’s clear that the county is forgoing approximately $11 million dollars property taxes by assessing the country club at a lower rate.

This amount of subsidy is baffling when considering that these clubs are only affordable to the ultra-rich. In order to join the Chevy Chase Country Club for example, members must pay approximately $80,000 in initiation fees. In addition, members must pay annual dues of $6,000 (coincidentally, this is almost equal to the annual property tax bill for the entire club!). These costs are out-of-reach for the typical Montgomery County family, which has a median household income of about $100,000.

Chevy Chase is already well-known for being one of the wealthiest neighborhoods in the United States, and Montgomery County residents are essentially subsidizing their expensive golf course.

It’s not hard to understand that this tax loophole is costing our local government millions in unrealized revenue, at a great benefit to the wealthiest of the wealthiest. What I struggle to understand is how Delegate Moon’s attempt to remove this policy was defeated in a 2-1 vote by his colleagues, most of whom run campaign platforms on “progressive values”.

{kind=link}

This article was updated on February 19 to correct some of the numbers used in the analysis.

Postscript:

The total assessed value is based on the value of the land vs. the value of the improvements (buildings). Since golf clubs are mostly open space, it’s not a fair apples-to-apples comparison to compare the total assessed value. In other words, the comparison above looked at what the club would pay if it were replaced with homes.

A more accurate comparison would look at the property taxes paid based on the value of the land. Based on a quick comparison of the assessed land value neighboring properties, it appears that the total effective subsidy for the entire club property is in the range of 5 to 8 million. If requested by readers, I can update this post later this week to more closely examine this consideration.

Thank you to everyone who wrote to me over the past weekend with critiques, corrections, and suggestions.